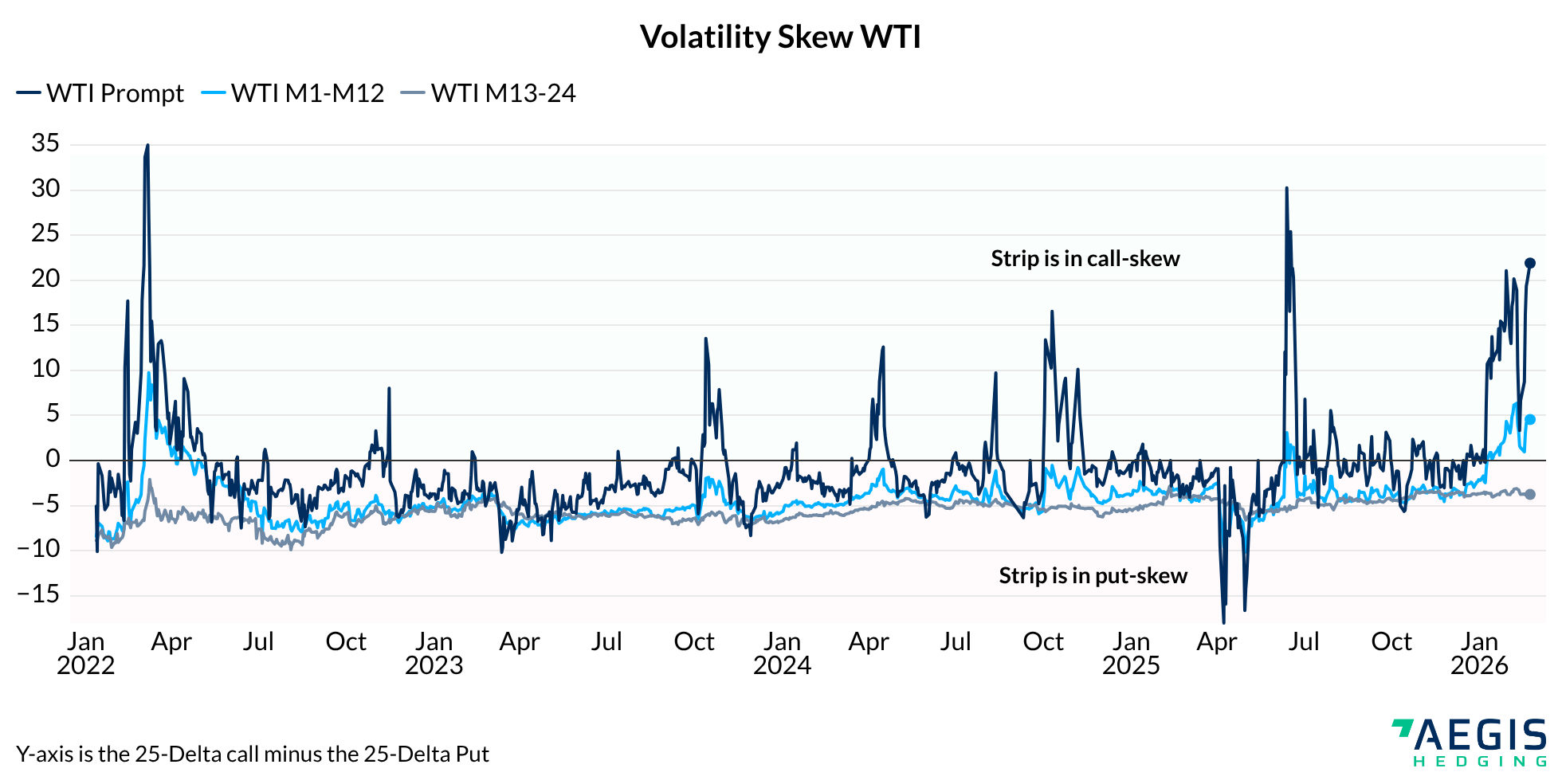

Oil options markets are sending a clear signal. Short-dated WTI skew has shifted decisively toward calls, reflecting a market paying up for upside protection. In crude, where skew often leans toward puts, that reversal is notable. The front of the curve has repriced sharply, marking one of the strongest call-skew readings since the Israel–Iran conflict in June 2025.

Why This Matters

The chart above plots the implied volatility differential between 25-delta calls and 25-delta puts. A positive reading indicates that upside calls are priced with higher implied volatility than comparable downside puts. In practical terms, investors are paying more for protection against a price spike than for protection against a decline.

The dark line represents prompt WTI and shows the most aggressive move. The lighter blue line captures the M1–M12 strip, effectively the next year of pricing. While it has also moved higher, the shift is more contained. The grey line, representing the 13–24 month strip, remains relatively stable and closer to neutral. That divergence across maturities is important. The options surface does not suggest structural tightness in longer-dated contracts. Instead, it points to concentrated near-term uncertainty and a meaningful increase in short-term tail risk.

Geopolitics and Front-End Volatility

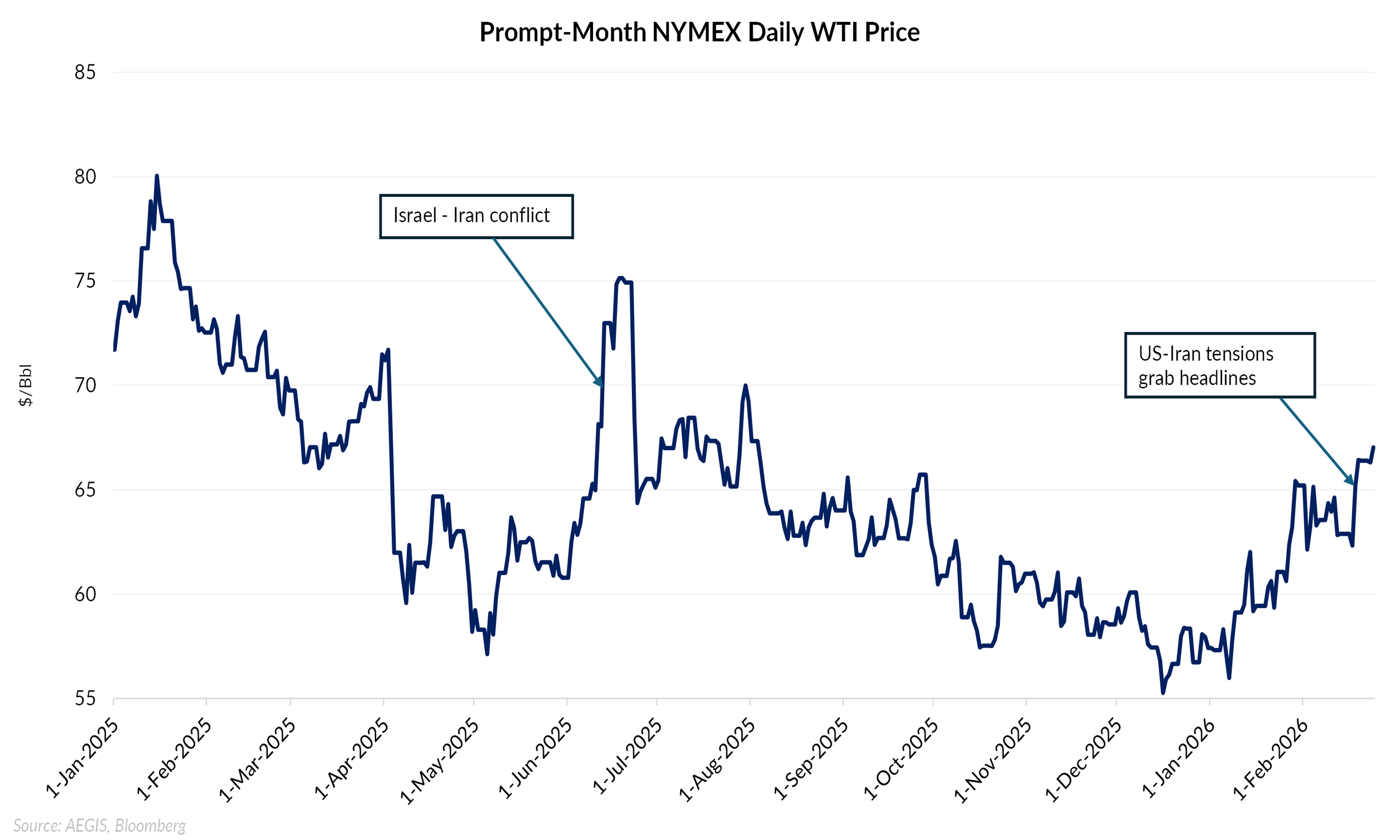

The move coincides with renewed US–Iran tensions. Increased military presence in the region and escalating rhetoric have produced sharp, headline-driven swings in prompt WTI. Similar patterns have emerged in past regional escalations, with prices rising as disruption fears intensified and retracing as those fears eased.

What This Means for Producer Collars

Because crude is typically in put-skew, producers selling calls as part of collar structures often receive less premium relative to the cost of downside protection. That dynamic has temporarily flipped.

With call-skew elevated, upside calls command richer premiums. Producers implementing collars or other option structures can capture materially greater value from selling call options. That additional premium can improve price floors or increase upside participation. Historically, as geopolitical uncertainty subsides, skew typically reverts toward its usual put bias. When that happens, the relative advantage in collar construction diminishes.

Conclusion

The oil options market is signaling elevated short-term geopolitical risk through unusually strong front-end call-skew. For producers, that shift creates a rare opportunity to secure stronger downside protection while maintaining additional upside participation.