The bullish story for natural gas over the next few years is mainly driven by the substantial increase in LNG export demand. However, this view is not without risks. An increase in global LNG supply, a decrease in global gas demand, or both could see the export price arbitrage between the US and global markets narrow. If the spread tightened enough, cargoes could be canceled, and reduced US exports would likely result in lower Henry Hub prices.

Global gas prices have typically been at a premium to Henry Hub in past years. This premium rose to extreme levels after Russia’s invasion of Ukraine in 2022 and the resulting stoppage of most Russian piped gas supply to western Europe. After these events, there was a swift ramp up in interest in the US around LNG export projects. Gas exports from the US had been increasing steadily since 2016.

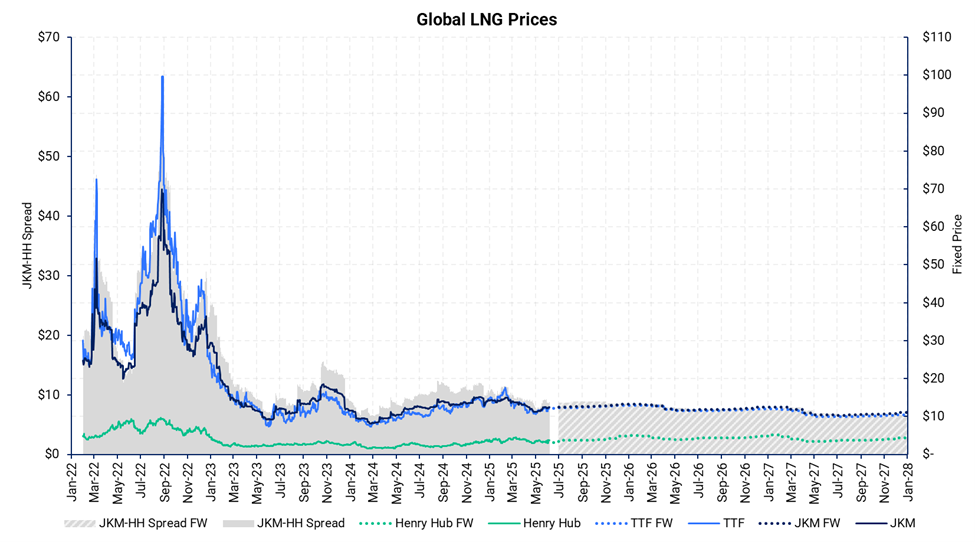

Since the onset of the Ukraine war, Europe has been able to make up for lost Russian gas supply via LNG imports, easing fears of an energy shortage. A series of warmer-than-average winters further helped to avoid shortages. This has led prompt Dutch TTF gas futures to fall substantially from a peak of more than $80/MMbtu in 2022, to current levels around $11/MMbtu, still more than double the price of prompt Henry Hub.

When looking at the forward curves for Henry Hub, TTF, and Japan-Korea Marker (JKM), it implies the arbitrage will remain open for the next few years. However, the price difference between Henry Hub and JKM or TTF becomes smaller into the future. The chart below shows Henry Hub, TTF, and JKM prompt prices along with their respective forward curves and the historical and forward spread between Hub and JKM. The downward slope in TTF and JKM forward prices is consistent with the continued buildout of global LNG export capacity and the increased supply available in the destination markets. Growing capacity in the US, Qatar, and Russia should keep global markets relatively well-supplied, reducing risk premiums.

Note: The grey area does not include costs

Outside of the spread between Hub and global markets, the cost of sourcing natural gas, liquefying it, and shipping it all factor into the export arbitrage calculation. According to Poten & Partners earlier this year, the cost of liquefaction has risen above $2.50/MMbtu. Shipping costs vary widely but are often cited as being in the range of $1.00-$3.00/MMbtu. Calculating a true breakeven is further complicated by the proliferation of long-term contracts, where some costs are sunk and not relevant to shipping the next cargo. Each export plant is different and will have varied operational costs. Putting it all together, the cost of feedgas, liquefaction, and shipping can add up to $6-$8/MMbtu.

This is not to say that if the forward or current spread begins falling below $8/MMbtu that we will start seeing lower LNG utilization, but the risk of cargo cancellations does increase. While the next few years look particularly bullish for Henry Hub, even a moderate reduction in LNG plant utilization could pose a risk to this view.