OPEC+ taps the brakes on supply hikes as market eyes glut

The WTI prompt-month contract rose $0.32 to settle at $59.75/Bbl on Friday, rebounding after three consecutive days of losses. As the risk premium from Russian sanctions begins to fade, the market’s attention has shifted back to the looming supply glut expected in 2026.

Over the weekend, OPEC+ announced another 137 MBbl/d supply increase for December, matching recent modest hikes. However, the group also signaled a pause in output hikes for the first quarter, citing weaker seasonal demand and growing uncertainty around the supply outlook. This marks the first halt in supply restoration since April and reflects OPEC+’s cautious approach as the market braces for a potential glut. As RBC’s Helima Croft noted, the pause is a prudent move given the unpredictable landscape ahead.

Meanwhile, non-OPEC producers are ramping up output as well. Brazil’s Petrobras is accelerating production from the world’s largest deep-water field, aiming to boost dividends even as crude prices hover near five-year lows and the market braces for a glut. Output from the Buzios field off Rio de Janeiro reached 1 MMBbl/d last month after the sixth floating production unit hit capacity ahead of schedule.

Geopolitical risks continue to influence the market landscape. Ukrainian drone attacks have temporarily suspended operations at Russian refineries and damaged tankers in the Black Sea, underscoring the vulnerability of global supply chains. At the same time, US and EU sanctions have caused Russia’s seaborne crude shipments to plunge by the most since January 2024, as key buyers avoid Moscow’s barrels. Refiners in China, India, and Turkey are pausing purchases of sanctioned cargoes and seeking alternative sources, pushing Russian crude at sea to more than 380 MMBbls. Despite these disruptions, Gunvor CEO Torbjorn Tornqvist commented that Moscow has historically found ways to bypass sanctions and expects that disrupted barrels will eventually find buyers.

Given the uncertainty surrounding the impact of sanctions, the market outlook will depend on the material effects of these measures, compliance with OPEC+ output targets, and the potential for further supply disruptions. For now, AEGIS maintains a bearish outlook as oversupply risks persist.

Crude Oil Factors

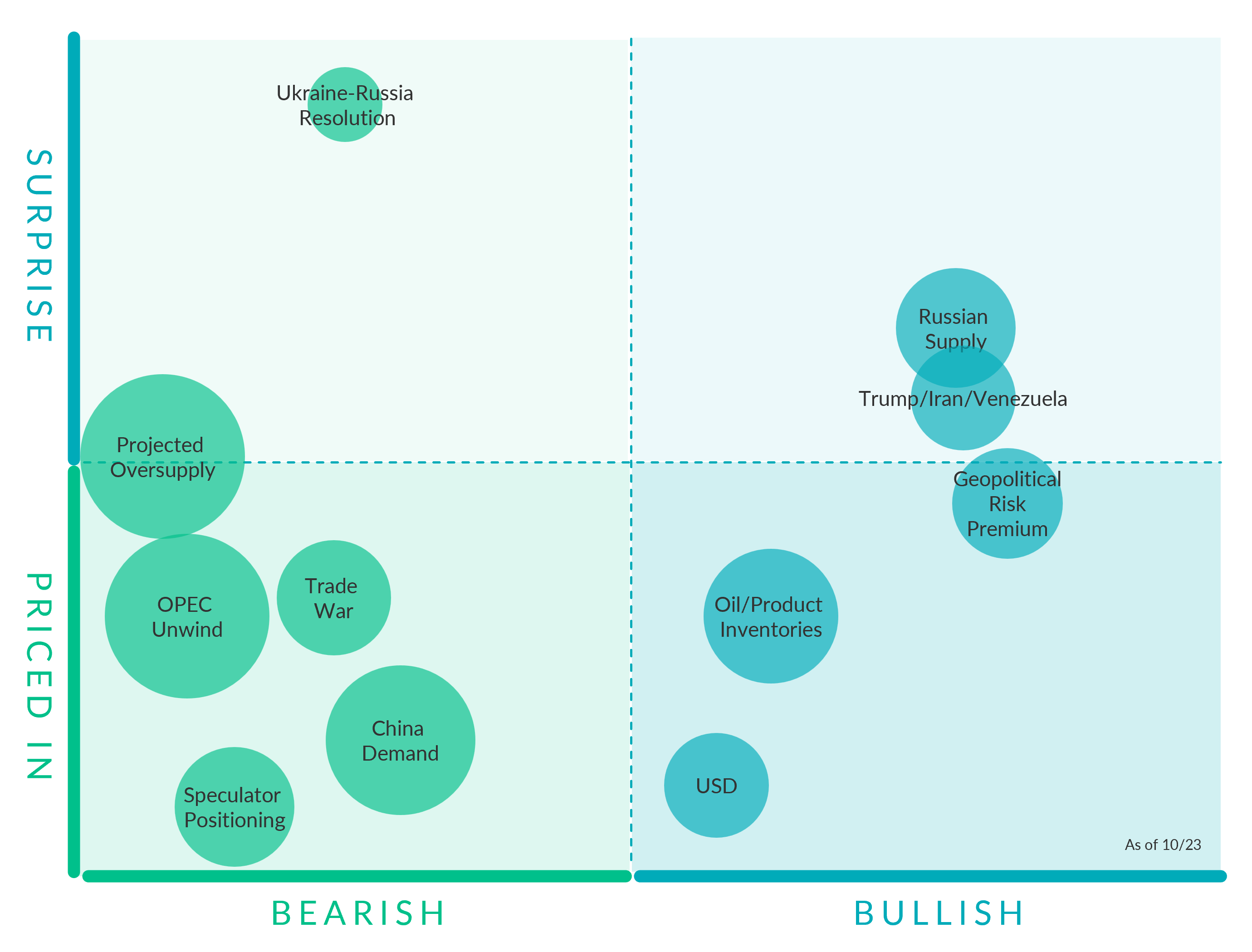

Geopolitical Risk Premium. (Bullish, Slightly Priced In) Geopolitical risks remain elevated. Ukrainian drone strikes targeted Russian oil infrastructure, temporarily suspending operations at the Tuapse refinery and damaging tankers in the Black Sea. These incidents underscore the vulnerability of supply chains and could act as bullish catalysts if disruptions persist or escalate.

Speculator Positioning (Bearish, Priced In) The latest CFTC data show that as of August 12, money managers reduced their net long in CME’s flagship NYMEX WTI contract to just 48,865 contracts, the smallest bullish position since April 2009. Meanwhile, trades of WTI done on the ICE exchange show money managers holding a net short of about 53,000 contracts. When the two venues are combined, overall positioning in WTI has slipped into net short territory for the first time on record.

Oil/Product Inventories. (Bullish, Priced In) The EIA reported a build of +5,202 MBbls in U.S. crude-oil inventories. In contrast, the market expected a draw of -247 MBbls as reported by Bloomberg. Inventories for the U.S. are now at a deficit of 5.90 MMBbls (-1.4%) to last year, and a deficit of 21.70 MMBbls (-4.9%) to the five-year average.

OPEC+ Quotas. (Bullish, Priced In) On June 2, OPEC+ announced its extension of 3.66 MMBbl/d cuts through December 2025. Additionally, the 2.2 MMBbl/d voluntary cuts from eight member countries will continue into Q3 2024 but will start to be reversed in October at a rate of 0.18 MMBbl/d per month. OPEC+ members agreed on September 5 to delay a planned gradual 2.2 MMBbl/d supply hike by two months, shifting the start to December. The group will add 0.19 MMBbl/d in December and 0.21 MMBbl/d from January onwards, with an option to adjust or pause these hikes depending on market conditions. The cartel also reaffirmed its compensation cuts of 0.2 MMBbl/d per month through November 2025, as members such as Iraq, Russia, and Kazakhstan have struggled to meet their original production quotas.

AEGIS notes that the global crude market would quickly build inventories without OPEC's support in reducing supply.

OPEC Unwind. (Bearish, Mostly Priced in) OPEC+ agreed to restore 137 MBbl/d for December, in line with the increases scheduled for October and November. Additionally, the group announced a pause in output hikes for Q1, citing typically weaker seasonal demand. Delegates noted the January pause reflects expectations of a seasonal slowdown

China Demand. (Bearish, Priced In) China’s onshore crude inventories declined to 1.17 billion barrels this week, down from a record 1.20 billion barrels in mid-August, according to data from Kayrros. The draws came from commercial stockpiles, partially reversing the country’s earlier stockpiling surge, a key factor that has supported global oil prices even as the broader market faces record oversupply.

USD (Bullish, Priced In) The Federal Reserve cut its benchmark interest rate by 25 basis points, the first cut since December 2024, and signaled that another 50 basis point cut could be coming by then end of 2025. If markets expect rate cuts or looser monetary conditions, the dollar tends to weaken. Oil is priced in dollars, so a weaker dollar lowers the “real” cost of oil for buyers using other currencies. This often boosts demand at the margin and supports prices.

Ukraine-Russia Resolution. (Bearish, Surprise) During President Trump’s Thursday meeting with Chinese leader Xi Jinping, Trump noted, “We didn’t really discuss oil.” The absence of strong pressure on Beijing to curb Russian crude purchases remains a key revenue stream for Russia’s war effort.

Trade War. (Bearish, Mostly Priced In) There has been an increase in tit-for-tat trade tension between the US and China, with China sanctioning the US unit of Hanwha Ocean Co., a South Korean shipping major, and warned of additional retaliatory actions against the industry. However, President Trump said high tariffs on China were “not viable,” suggesting potential for de-escalation even as broader tensions remain elevated.

Projected Oversupply. (Bearish, Mostly Surprise) The IEA’s latest Oil Market Report projects global crude supply to outpace demand by nearly 4 MMBbl/d next year. The forecasted overhang is about 18% larger than last month’s estimate, reflecting OPEC+’s ongoing supply revival.

Trump/Iran/Venezuela. (Bullish, Slight Surprise) Tensions in South America are escalating as reports surfaced stating the US is looking to target Venezuelan military sites. According to OPEC secondary sources, Venezuela's crude production in September was 967 MBbl/d.

Russian Supply. (Bullish, Slight Surprise) Due to the latest sanction on Rosneft and Lukoil, analysts at Rystad Energy estimate 500–600 MBbl/d of Russian output could be curtailed, forcing Moscow to rely more heavily on shadow tanker fleets and Chinese buyers. However, the extent of any disruption remains uncertain, and it may take time to gauge how material the impact truly is.

Commodity Interest Trading involves risk and, therefore, is not appropriate for all persons; failure to manage commercial risk by engaging in some form of hedging also involves risk. Past performance is not necessarily indicative of future results. There is no guarantee that hedge program objectives will be achieved. Certain information contained in this research may constitute forward-looking terminology, such as “edge,” “advantage,” ‘opportunity,” “believe,” or other variations thereon or comparable terminology. Such statements and opinions are not guarantees of future performance or activities. Neither this trading advisor nor any of its trading principals offer a trading program to clients, nor do they propose guiding or directing a commodity interest account for any client based on any such trading program.