To quickly access the page content, please click on the links below.

|

TRADE DATE |

HUB |

PRODUCT |

STRIP |

SETTLEMENT PRICE |

PERCENTAGE DIFFERENCE FROM DEC 22 |

|

8/31/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-22 |

145.30000 |

100% |

|

8/31/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-23 |

101.75000 |

70% |

|

8/31/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-24 |

85.50000 |

59% |

|

8/31/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-25 |

88.20000 |

61% |

|

8/31/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-26 |

74.20000 |

51% |

|

8/31/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-27 |

76.60000 |

53% |

|

8/31/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-28 |

73.05000 |

50% |

|

8/31/22 |

NYISO J Off-Peak |

Off-Peak Futures (50 MW) |

Dec-29 |

68.35000 |

47% |

|

8/31/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-22 |

173.60000 |

100% |

|

8/31/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-23 |

137.65000 |

79% |

|

8/31/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-24 |

111.35000 |

64% |

|

8/31/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-25 |

105.10000 |

61% |

|

8/31/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-26 |

91.20000 |

53% |

|

8/31/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-27 |

95.35000 |

55% |

|

8/31/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-28 |

90.40000 |

52% |

|

8/31/22 |

NYISO J |

Peak Futures (1 MW) |

Dec-29 |

89.45000 |

52% |

|

8/31/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-22 |

123.50000 |

100% |

|

8/31/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-23 |

78.35000 |

63% |

|

8/31/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-24 |

58.45000 |

47% |

|

8/31/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-25 |

56.35000 |

46% |

|

8/31/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-26 |

59.30000 |

48% |

|

8/31/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-27 |

63.30000 |

51% |

|

8/31/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-28 |

63.50000 |

51% |

|

8/31/22 |

PJM PSEG Zone DA |

Peak Futures (1 MW) |

Dec-29 |

64.25000 |

52% |

|

8/31/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-22 |

109.10000 |

100% |

|

8/31/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-23 |

59.45000 |

54% |

|

8/31/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-24 |

47.00000 |

43% |

|

8/31/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-25 |

42.85000 |

39% |

|

8/31/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-26 |

46.25000 |

42% |

|

8/31/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-27 |

47.35000 |

43% |

|

8/31/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-28 |

48.00000 |

44% |

|

8/31/22 |

PJM PSEG Zone DA Off-Peak |

Off-Peak Futures (1 MW) |

Dec-29 |

48.70000 |

45% |

New York seeks more Tier 2 RECs. On August 16th, The New York State Energy Research and Development Authority (NYSERDA) launched its third Tier 2 RECs solicitation for in-state renewable energy generators that have been operational since 2015. The target volume and maximum bid price are kept confidential. Only private, run-of-river hydro projects and onshore wind farms are eligible for solicitation. Proposal has to include fixed RECs price and annual output in MWh. The winners will be selected according to the lowest available bid price until the target volume is reached or the maximum bid price is exceeded. Winning projects will enter a three-year agreement with the state from January 1st, 2023, to December 31st, 2025. All RECs surplus generated above the contracted amount will belong to the developer. Final proposals are accepted till September 15th, and winners are announced in October.

New Jersey provides TREC extensions. On August 17th, State regulators gave more time to public and “subsection t” projects to link with the transition incentive solar program. The New Jersey Board of Public Utilities (BPU) gave up to six-month extension if the project continues to show progress towards coming on line. The extensions provide developers a chance to receive the transition renewable energy certificates (TRECs), which are bought for a baseline of $152/MWh, compared with $70-$100/MWh incentives under the new program. Transition initiative registered with more than 320 public solar projects, which totaled the capacity of 176MW. The number includes 23 public entities covered under the initiative, allowing NJ government entities to upgrade their facilities by using savings from energy-related developments. For the “subjection t," a total capacity of 500MW among 30 projects is seeking eligibility for the TREC. However, the board has conditionally certified 10 of them, with a total capacity of 117 MW. Moreover, the board has rejected petitions from the small projects under the 1MW capacity as they have not seemed mature enough for the transition program and have not demonstrated significant circumstances for the delay.

New Jersey solar capacity growth. The New Jersey Clean Energy Program reported on August 24th that the state added 26MW in the new solar capacity in July. Therefore, improving the initial figures of 10.9MW and 18.6MW logged for May and June. However, it is still significantly less than the 41MW initially reported in April. One-fourth of July capacity, around 6MW, went to the ADI initiative, the fixed-price portion of the state's new SREC-II incentive program. The remaining 20MW of the new capacity is fed into the state's transition incentive program, which issues transition renewable energy certificates (TRECs) at a base price of $152/MWh for a 15-year period and requires the state's four electricity distributors to buy the credits. No capacity went towards the legacy solar renewable energy certificate (SREC) program. The state has increased its solar fleet by 206.6 MW throughout 2022, to the total of 4,067 MW.

New Jersey’s Environmental Justice rules. The public comment period closed on September 4th. The Department is still aiming to adopt the rule by December 31st, 2022. Full proposal could be found here.

Improvement in PJM generation of wind and solar. PJM issued 7 mn RECs in July compared with 6.9 mn RECs in the previous year. 57.6 mn credits were created throughout the first seven months of 2022. That is a 9.3% increase from 52.7 mn RECs generated during the same period in 2021. There were 1.7 mn RECs sourced from wind and 1.9 mn from solar, which led to the second consecutive month when solar volume outperformed wind. Year to date, solar credits reached 11.4 mn RECs and wind ones – 22.4 mn RECs. However, only 11,100 RECs were generated from the geothermal projects. Moreover, hydropower RECs generation continues to be sluggish as a 16.9% drop is seen compared with the same period in 2021. Landfill gas RECs dropped by ~21% to 1.5 mn credits in January – July 2022 compared to the previous year.

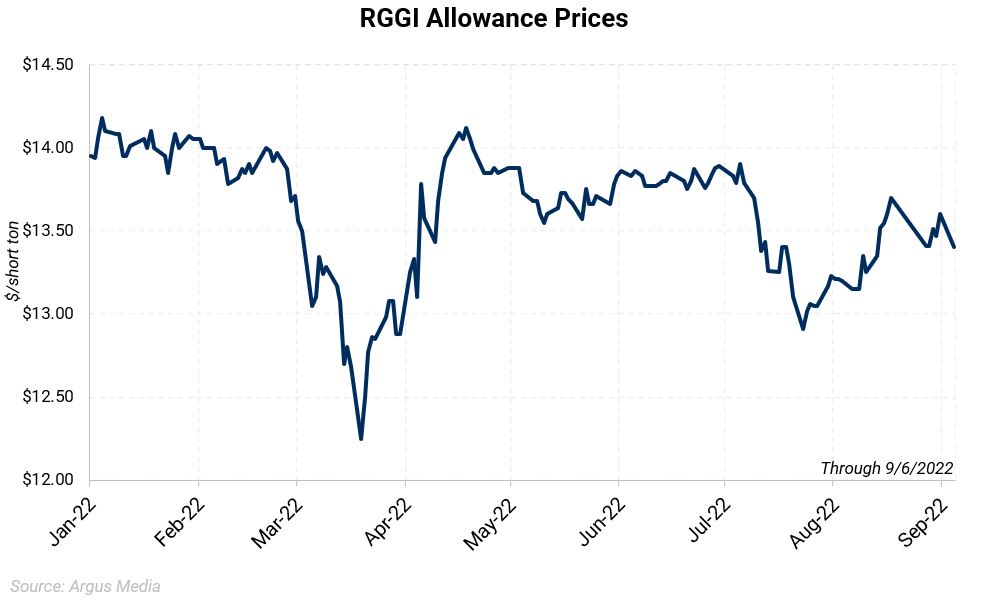

Pennsylvania is not participating in the next RGGI auction on September 7th. As the legal uncertainty is still surrounding Pennsylvania’s efforts to join the program, the state will not participate in the next RGGI CO2 allowance auction. Consequently, around 16mn allowances will be removed from the sale. The decision was made after the state Supreme court did not lift the injunction, which stands in the way of the state's participation in the program. As a consequence, the future auction will suggest only 22.4 mn allowances from the remaining 11 states at a reserve price of $2.44/short ton. Furthermore, the auction's cost-containment reserve will drop to 11.6 mn short tons. (reserve would be used if the clearing price reaches $13.91/short ton). There are three lawsuits against Pennsylvania’s wish to join the eastern US power plant cap-and-trade program involving Republican state lawmakers, coal groups, and the owners of natural gas-fired generators. The Commonwealth Court is planning to have hearings on September 14th and in November to discuss the RGGI rule's legality.

Pennsylvania’s deadline for Q4 RGGI Allowance Auction. DEP established a deadline for the State’s Supreme court to lift the injunction to be able to participate in the December auction. Pennsylvania will not offer 15.6 million allowances on December 7th if the RGGI regulation is not reinstated by October 23rd. The preliminary injunction was issued on July 8th, a week after the state joined the program. The court orders already prevented Pennsylvania from participating in the Q3 auction.

RGGI trading activity is up in Q2. Futures trading volume reached 107 million allowances in Q2 2022, a 35 million allowances increase compared to Q1 2022 and a 50 million increase to Q2 2021. Furthermore, RGGI futures and options open interest increased by 43%, from 79 million allowances in Q1 2022 to 113 million allowances in Q2 2022. Option-implied volatility fell significantly to the 39% average compared to the 49% in Q1 2022. In the year's second quarter, the average allowance future price on ICE was $13.81/short ton, a 25-cent increase from the average price in the first months of this year. Around 49% of RGGI allowances in circulation are held for compliance purposes.

Virginia targets to leave RGGI by end of 2023. The state is planning to issue a notice of starting the legal action to leave the RGGI program by the end of 2023. Leaving the program by December 2023 would match the end of the program's current three-year compliance period and the contract's end date between Virginia and the RGGI program. At the August 31st Air Pollution Control Board meeting, it was stated that the standard regulatory process would be followed instead of the earlier proposed "immediate" one.

Questions? Contact our team for more information: environmental@aegis-hedging.com

CONFIDENTIAL – UNAUTHORIZED THIRD-PARTY DISTRIBUTION PROHIBITED